Since his return to office in January, President Donald Trump has called on Federal Reserve Chairman Jay Powell to cut interest rates which Powell and the Fed’s Board of Governors have refused to do. In typical child-like behavior when he doesn’t get his way, Trump has hurled insults at Powell calling him a “stupid person,” “too late Powell,” and a “numbskull.”

Trump’s juvenile attacks, although misplaced, have been quite humorous and a welcome change in tone to the respect, reverence, and almost deification that previous Presidents, Congressmen, and the financial press heap on Federal Reserve Chairmen.

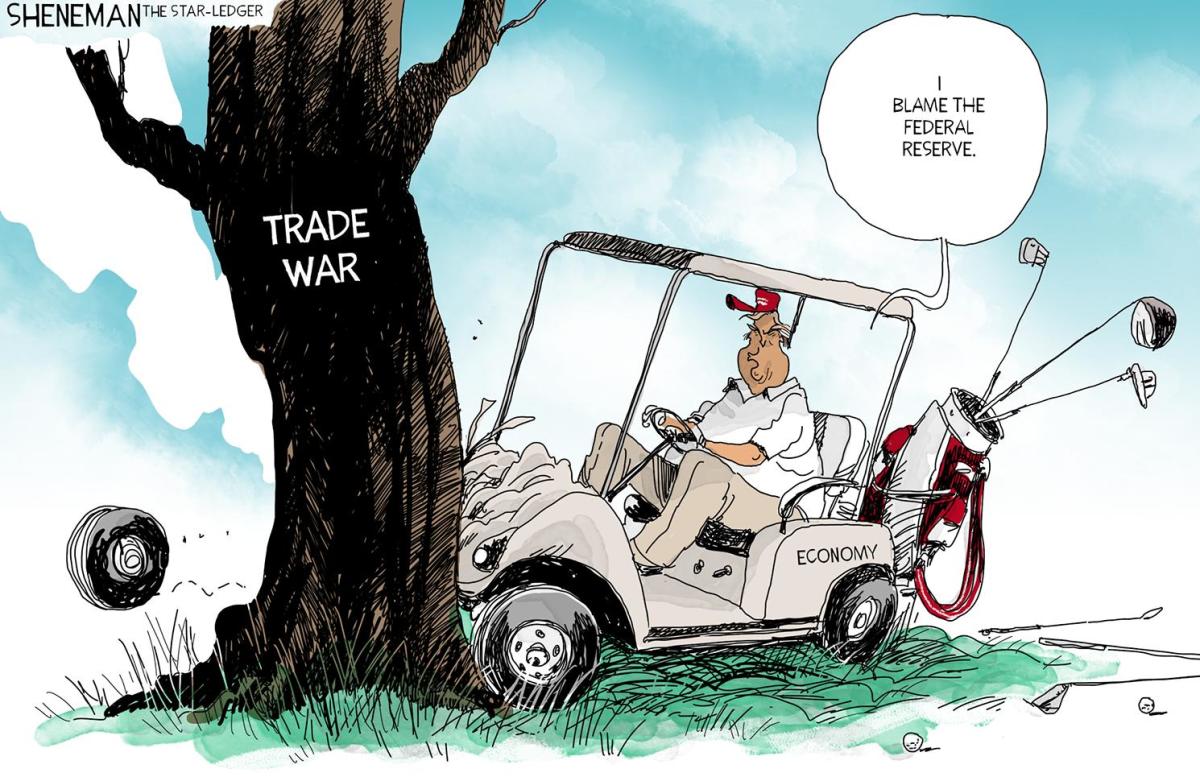

Unfortunately, as with all his policies, Trump’s megalomania is on display. After the Fed’s June meeting when it once again decided to leave rates unchanged and indicated that there might be only one rate cut in 2025, Trump again slammed Powell and suggested that “Maybe I should go to the Fed. Am I allowed to appoint myself to the Fed.?” *

While Trump’s ridiculing the head of one of the sacred cows of America’s ruling establishment is welcomed, his crazed notion of putting himself, and presumably future presidents, in charge of monetary policy does not offer any viable alternative to the debt crisis that is staring the nation in the face with the U.S. in the hole in excess of now some $37 trillion.

Although Trump’s blasting of Powell has provided some comic relief from the dire economic conditions which confront the U.S., in reality both the president and the Fed Chair are wrong over interest rate policy although, in this case, Powell is less wrong. Like most of Trump’s kooky ideas – taking over Greenland, making Canada the 51st state – not only is the slashing of interest rates counterproductive, but the idea of giving the executive branch of government control of monetary policy would turn the nation into a complete dictatorship.

Powell, too, has been mistaken in his policy of holding rates steady. Interest rates, in fact, are too low and need to be higher. At current levels, rates are too “accommodative” as price inflation remains above the Fed’s 2% target. Of course, in reality prices are rising at a much briskier pace than official government estimates.

Hiking rates would encourage savings and discourage consumption both of which would put downward pressure on consumer prices. If Trump wants to achieve his goal of a reindustrialized America, there needs to be an increase in savings. Production of goods takes place over time and without savings to fund the construction of factories, the purchase of machines and equipment, and the payment of wages, there can be no economic growth.

Trump wrongly believes that lower rates will spur economic growth. Sustained prosperity can only take place through savings and investment not money creation via credit expansion which the president is a fan of.

More fundamentally, both Trump and Powell are wrong: interest rates should not be set by governments or monetary authorities, but be determined by market forces – the aggregate decision making of individuals on how much to save or how much to consume their income. Concomitant with non-state involvement with the setting of interest rates, a return to a metallic monetary standard would prevent price inflation which would make saving more attractive.

Another reason why Trump wants lower rates is that servicing the mammoth U.S. debt would be somewhat more palatable. His “big, beautiful bill,” working its way through the Senate, will need to be financed. Lower rates would reduce the government’s borrowing costs. This irresponsible argument was also made by former Federal Reserve Chair and later Treasury Secretary Janet Yellen.

Since Donald Trump has no ideological core that shapes his world vision, his outlook and policies are more often than not based on what affects him personally or who strokes his ego or lines his pockets. The proper monetary policy for the nation is not to cut interest rates, but to raise them and reduce the national debt through spending cuts. While there would certainly be short-term pain from such a policy, eventually matters would turn around and economic activity would be placed on a sound footing.

Ultimately, if sound money is ever to return to America and the Western world, its control must be taken away from central banks and the influence of mercurial politicians. The creation of money, its distribution, authenticity, and safe keeping should be left up to a decentralized non-governmental arrangement.

*Tyler Durden, “Trump Slams ‘Stupid’ Powell: ‘I Think He Hates Me. I Call Him Every Name in the Book to Try and Get Him to Cut,’” Zero Hedge, 18 June 2025. https://www.zerohedge.com/markets/trump-slams-stupid-powell-i-think-he-hates-me-i-call-him-every-name-book-try-and-get-him

Antonius Aquinas@AntoniusAquinas